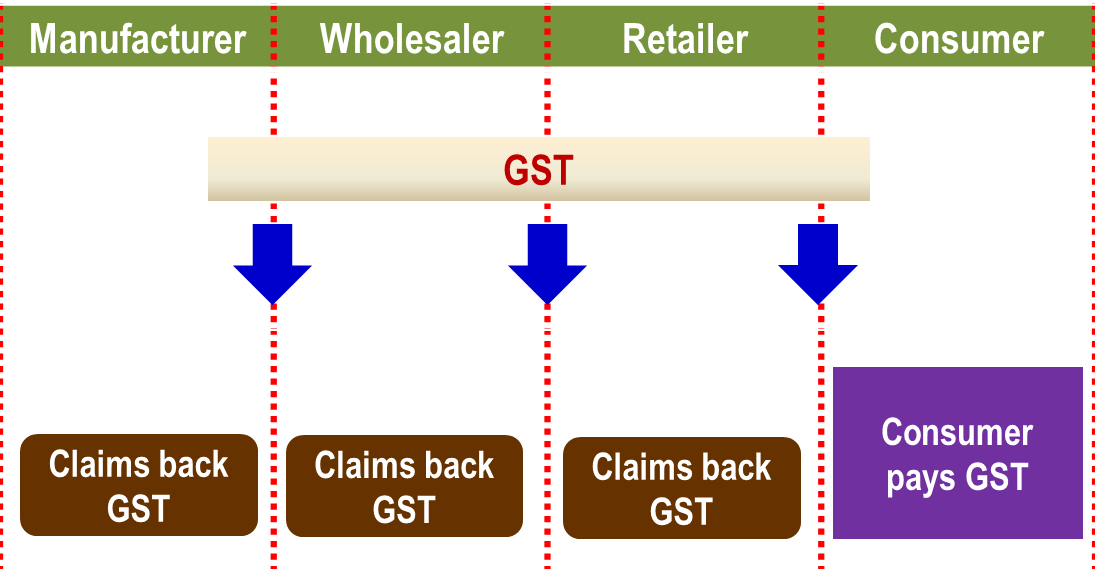

Goods and Services Tax or GST is a consumption tax based on value-added concept. Unlike the present sales tax or service tax which is a single stage tax, GST is a multi-stage tax. Payment of tax is made in stages by intermediaries in the production and distribution process. The tax itself is not a cost to the intermediaries since they are able to claim back GST incurred on their business inputs.

GST is imposed on goods and services at every production and distribution stage in the supply chain including importation of goods and services.

No, it is a tax to replace the current Sales Tax and Service Tax (SST).

Many countries have adopted GST/VAT because they are dissatisfied with their consumption tax structure. This dissatisfaction falls broadly into one and possibly all of the following categories:

- The existing consumption sales tax is unsatisfactory

- A reduction in the rate other taxes is sought

- The existing tax system has not kept pace with the development of the economy

In the case of Malaysia, the introduction of GST is part of the overall Government tax reform programme towards making the taxation system more efficient, effective, transparent, business friendly and capable of generating a stable source of revenue. GST is to replace the current consumption tax comprising of SST.

Based on the study conducted by the Ministry of Finance, GST can overcome the various inherent weaknesses under SST namely:

- Tax cascading and tax compounding

- Issue of transfer pricing and value shifting

- No complete relief of the tax on goods exported

- Discourages vertical integration

- Bureaucratic red tape

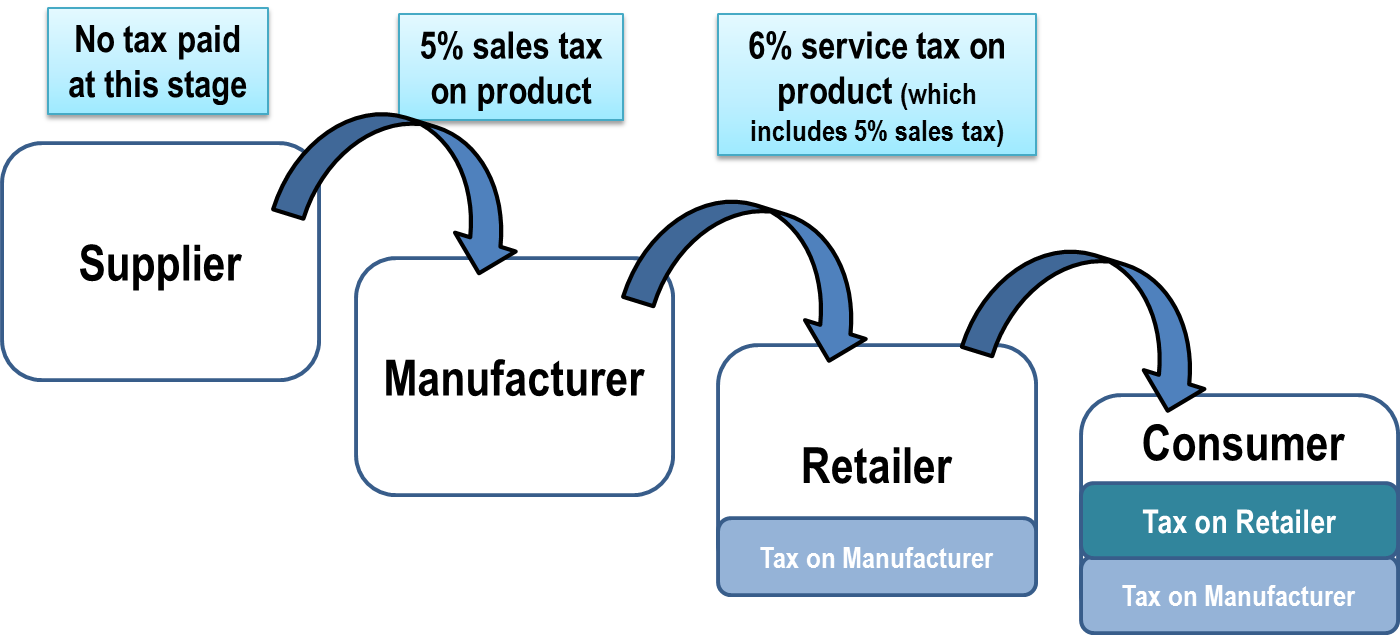

Diagram 1: Cascading effect (SST)

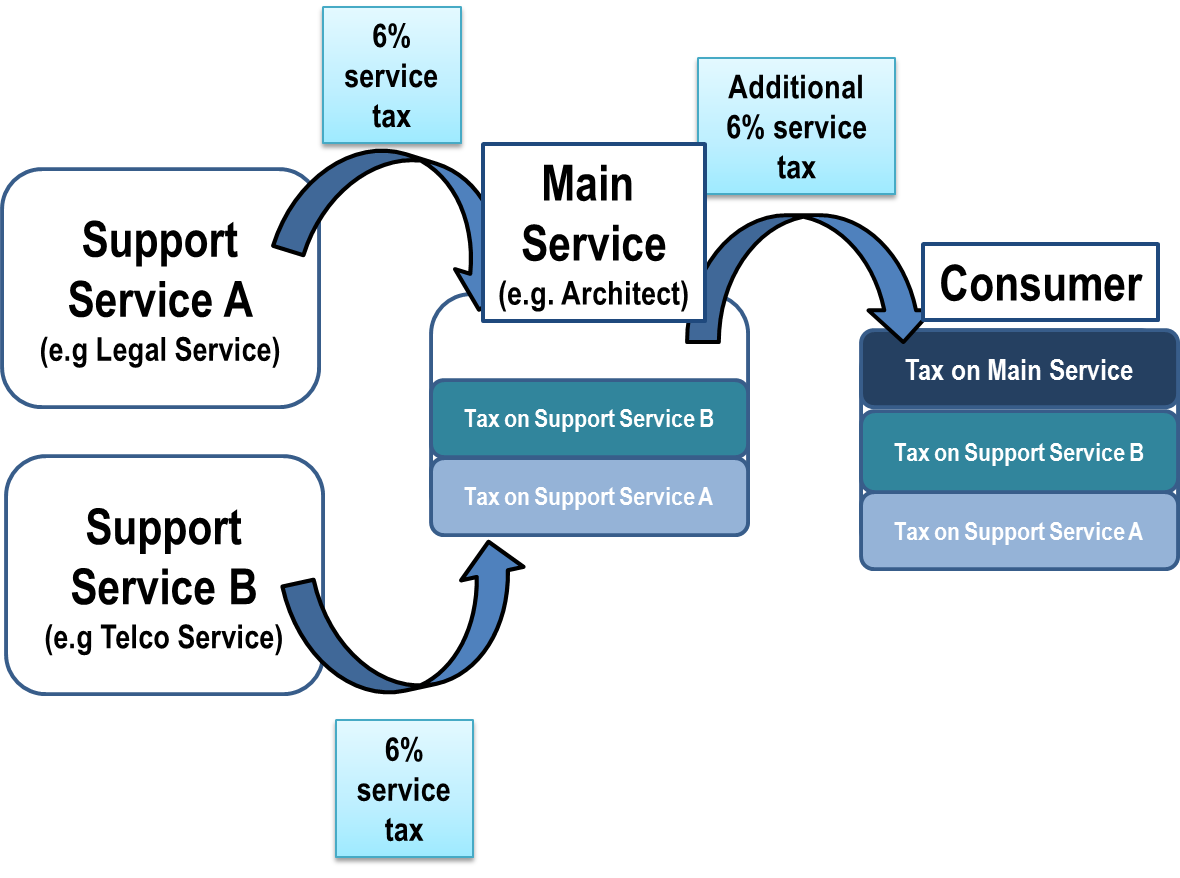

Diagram 2: Cascading effect (service tax)

Why now? Today there is a wealth of experience to tap into. In other

words, the chance of success in implementing GST is high as there is

much experience for Malaysia to draw upon them around the world in

designing the system. Over the years, GST/VAT has been adopted as a

main form of taxation. Currently, more than 160 countries have

implemented GST/VAT.

GST is a better tax system. It is more transparent, efficient,

effective, self policing and less bureaucratic. GST would eliminate

double taxation under the current SST. Consumer will pay fair prices

for most goods and services compared to SST.

|

|

Before GST (SST)

|

GST

|

|

Sales by manufacturer (juices)

|

2.00

|

2.00

|

|

Tax

|

(10% sales tax) 0.20

|

(6% GST) 0.12

|

|

Price paid by hotel

|

2.20

|

2.12

|

|

Input tax credit

|

nil

|

-0.12

|

|

Cost to hotel

|

2.20

|

2.00

|

|

Mark up (100%)

|

2.20

|

2.00

|

|

Selling price before tax

|

4.40

|

4.00

|

|

Tax

|

(6% service tax) 0.26

|

(6% GST) 0.24

|

|

Price paid by consumer

|

4.66

|

4.24

|

|

|

0.46

|

0.36

Savings (0.46 – 0.36) = 0.10

|

For businesses, they are able to reduce their cost of doing business

since they are able to claim GST incurred on their business inputs.

For example, under the current taxation system, manufacturers are

not allowed to claim service tax on telecommunication, accounting

and legal services and sales tax on indirect inputs such as office

equipment and furniture. These taxes are embedded into the price of

the goods sold. Hence, the cost of doing business increases. Under

the GST system, any GST incurred on acquisition is claimable and is

not a cost to businesses.

As such, Malaysian exports will become more competitive in the

global market as no GST is imposed on exported goods and services.

This will strengthen our export sector which would contribute to the

economic growth of the country.

Not all goods and services will be subjected to GST. Certain basic

food and amenities such as rice, poultry, fish, meat, vegetable,

sugar, flour and cooking oil are free from tax. Meanwhile, the sales

and rental of residential and agricultural properties and services

like private health and education as well as public transportation

are exempted from GST.

No. To make our exports more competitive, GST on exports will be

zero-rated and the exporter can recover all the input tax incurred

in the course of his business.

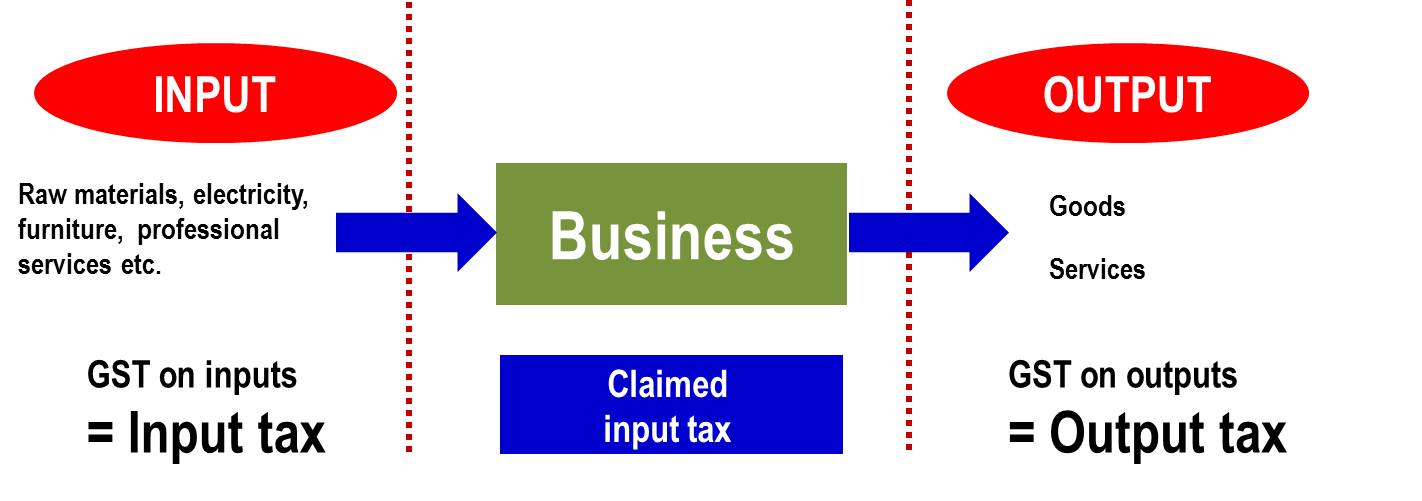

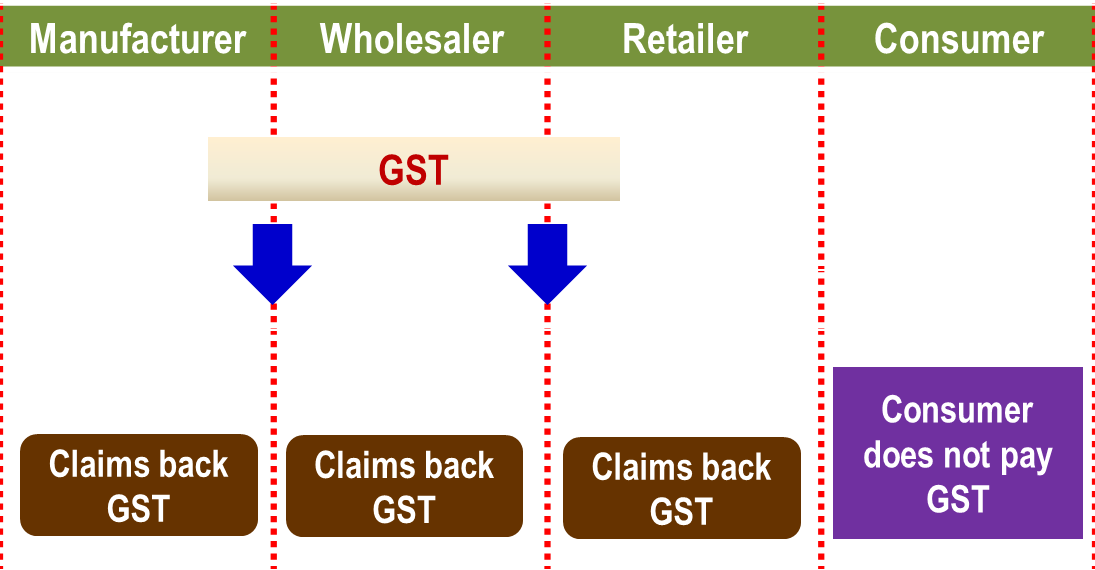

GST is a tax charged on the supply (including sales) of goods and

services made in Malaysia and on the importation of goods and

services into Malaysia. Even though GST is charged on the sales

price of the goods or services, the amount to be remitted to the

Government is only on the value added to the goods or services at

each level of the distribution/supply chain. The value added is the

value that a producer (whether a manufacturer or distributor, etc)

adds to its raw material or purchases before selling the new or

improved product or service. To enable this, GST adopts a credit

offset mechanism whereby GST charged on the output of the business

(for example, sale of product manufactured or services supplied) is

offset against the GST paid on the goods or services acquired as

inputs (for example, raw materials or utilities to be used in

manufacturing) by the business. GST charged on output is called

output tax. Whereas, GST incurred on acquisition is called input

tax. This offsetting mechanism is to ensure GST paid by businesses

are recoverable and thus help to reduce the costs of doing business.

Diagram 1: Input and output tax

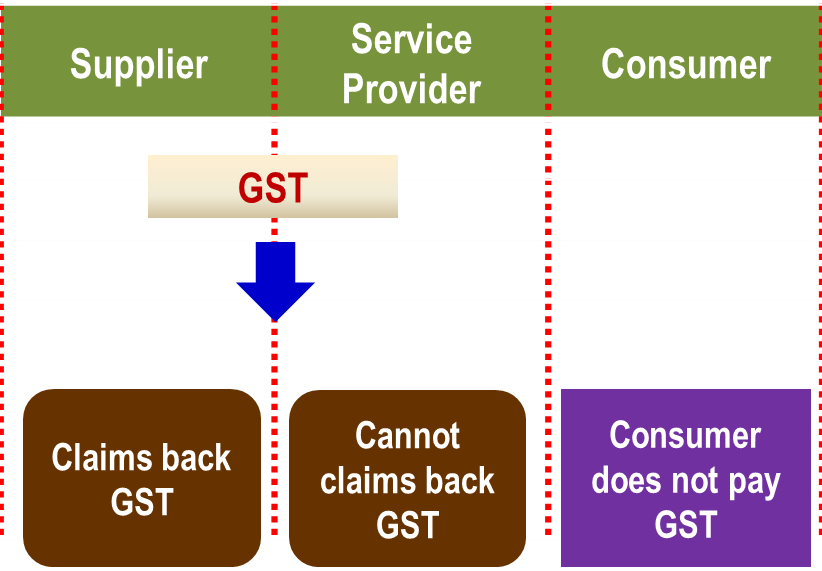

There are three types of supplies listed under GST which are:

- Standard rated supplies are taxable supplies of goods and services which are subject to a positive rate

- Zero rated supplies are taxable supplies which are subject to a zero rate that is not liable to GST at the output or input stage

- Exempt supplies are non taxable supplies which are not subject to GST at the output stage that is, when supplied to the consumer. However, the GST paid on input by the businesses cannot be claimed as tax credit

Below is an illustration showing how GST works:

Diagram 2: Standard rated supply

Diagram 3: Zero-rated supply

Diagram 4: Exempt supply

The following are the GST rate among the ASEAN countries:

|

Countries

|

Year of Implementation

|

Initial Rate (%)

|

Current Rate (%)

|

|

Indonesia

|

1984

|

10

|

10

|

|

Thailand

|

1972 |

10 |

7

|

|

Singapore |

1993 |

3

|

7

|

|

Philippines

|

1998

|

10

|

12

|

|

Cambodia

|

1999

|

10

|

10

|

|

Vietnam

|

1999

|

10

|

10

|

|

Laos

|

2009

|

10

|

10

|

In the early 1990’s there was an equal contribution to revenue between

direct and indirect tax for example in 1990 the contribution from direct

tax is 35.2% and indirect tax is 36.7%. However, with trade

liberalisation policies in the 1990’s this proportion has changed

substantially and in 2012 contribution from direct tax was 56.4% and

indirect tax 17.2%. Studies by economic experts have shown that over

reliance on a particular tax will have an adverse effect on the nation’s

financial position. Currently, Malaysia relies heavily on direct tax and

petroleum revenue and now it is an appropriate time for the Government

to undertake an overall tax reform to correct the imbalances. One of the

measures is to introduce GST which is a more efficient system compared

to the current tax system.

In 2005 budget, the Government had announced the introduction of GST. However, it was deferred to a later date. In December 2009, the GST Bill was tabled for the First Reading in the Dewan Rakyat and in 2010, the implementation of GST was postponed due to:

i. Enable the Government to engage inclusively with all segments of

the rakyat

ii. Take into account the interest and welfare of the society to

ensure the implementation of GST is well received

Notwithstanding the postponement, the Government recognises the importance of GST in ensuring a strong and sustainable fiscal position to support the long term economic growth.

Today there is a wealth of experience to tap into. In other words, the chance of success in implementing GST is high as there is much experience for Malaysia to draw upon them around the world in designing the system. Over the years, GST/VAT has been adopted as a main form of taxation. Currently, more than 160 countries have implemented GST/VAT.

Economists in Malaysia agree that now is the appropriate time for the

Government to implement GST. There are also quarters who feel that GST

should be implemented once Malaysia achieves the developed nation

status. From the point of the tax system, the main concern is to

overcome the inherent weaknesses in the current sales tax and service

tax system. Currently, there are more than 160 countries implementing

GST. The implementation of GST will contribute towards Malaysia

achieving a high income status.

At present, imported goods are subject to import duty and sales tax

unless exempted. Under GST, imported goods will still be subject to

import duty but sales tax will be replaced with GST. As to whether the

imported goods will be cheaper or more expensive will depend on a number

of factors besides the GST rate.

The Government has given businesses ample time to be ready for GST.

Education, training, awareness programs and advisory visits regarding

GST implementation have and will be conducted on an on going basis.

Businesses will be allowed to register early before GST enforcement

date. Prior to GST implementation, the Government will carry out pilot

runs on the systems. The Government has set up a Customs Call Centre

(CCC) to enable the public to make inquiries on GST and the existance of

the GST Portal will disseminate information on GST to ensure high

compliance when GST is implemented.

Yes, the Government has prepared itself fully to implement GST. The GST

legislation, infrastructure, computer system, personnel, and all process

and procedures are in place to implement GST.

The introduction of GST in Malaysia is to replace the current consumption tax (Sales Tax and Service Tax) which has many weaknesses. GST is part of the overall tax reform to make the taxation system more effective, efficient, transparent, business friendly and capable of generating a more stable source of revenue. In the long run, a more effective and efficient tax system will help in reducing the fiscal deficit in Malaysia.

Currently the Ministry of Finance is conducting a series of

awareness program on GST to the public and businesses. The aim of

this awareness program is to help the public and business to have a

better understanding on the proposed GST model in Malaysia, the

mechanism and steps taken by the Government to overcome issues

raised concerning GST.

The people need to know that GST is charged and collected on all

taxable goods and services produced in the country including

imports. Only businesses registered under GST can charge and collect

GST. GST collected on output must be remitted to the Government.

However, businesses are allowed to claim the input tax credit.

As far as the rakyat is concerned they only need to pay GST if they

consume those goods or services. If not, they are not affected by

GST.

There will be a positive impact on the economy due to the following:

- Reduction in business costs:

- Special schemes to alleviate cash flow problems

- Credit offset mechanism

- Can claim the input tax due based on the invoice produced

- Lead to more competitive pricing

- Makes our export more competitive as exports are to be zero-rated

- Increase in Gross Domestic Product

- Reduce shadow economy activities

- It is a tool to manage the economy eg

tourist refund scheme is proposed as a means to boost the tourism

industry and tourism spending in the country, exports are zero-rated

to make our goods more competitive globally.

There might not be a reduction in consumption due to:

- Prices of certain goods and services might be lower

- Change in consumption pattern. GST works on the

affordability concept. Consumers have to decide on which goods or

services to buy and GST is only incurred when the goods or services

are consumed. They may divert more of their expenses towards

essential goods and services rather than on luxury goods

- A lot of basic necessities are not subject to GST

- GST is a replacement tax

- Input tax credit mechanism should

reduce business cost.